Bookkeeping is the foundation of financial management for any small business. In the UAE, accurate bookkeeping helps business owners track performance, manage cash flow, prepare for VAT and corporate tax obligations, and make informed decisions.

Many small businesses start with informal recordkeeping methods, but as transactions increase, bookkeeping becomes a critical business function. Missing invoices, unreconciled bank accounts, and incomplete tax records can create compliance risks and make it difficult to understand the true financial position of the business.

Understanding the basics can help UAE business owners maintain organized records and avoid common mistakes.

What Is Bookkeeping and Why Does It Matter?

Bookkeeping is the process of recording, organizing, and maintaining a company's financial transactions. These transactions include:

- Sales revenue

- Customer payments

- Supplier invoices

- Business expenses

- Payroll payments

- Bank transactions

- VAT-related entries

The purpose of bookkeeping is to create an accurate financial record of business activity. Without reliable records, it becomes difficult to prepare financial statements, calculate taxes, monitor profitability, or identify cash flow issues.

For UAE SMEs, bookkeeping also supports compliance with Federal Tax Authority requirements and helps maintain records that may be requested during audits or tax reviews.

The Core Financial Records Every UAE Business Should Maintain

Small businesses should keep complete and organized records of all financial activity.

Key records include:

Sales Invoices

Every sale should be documented with a properly issued invoice. Businesses registered for VAT must ensure invoices meet UAE VAT requirements where applicable.

Purchase Invoices and Expense Receipts

Supplier invoices, receipts, and expense documentation should be retained and categorized correctly. Missing expense records can create difficulties when preparing tax filings and supporting deductions.

Bank Statements

Business bank statements provide an independent record of transactions and are essential for verifying bookkeeping accuracy.

Customer and Supplier Records

Maintaining updated accounts receivable and accounts payable records helps businesses track outstanding payments and manage working capital.

Payroll Records

Businesses with employees should maintain salary records, leave records, employment contracts, and payroll documentation. Where applicable, payroll processing should align with UAE labour regulations and Wage Protection System requirements.

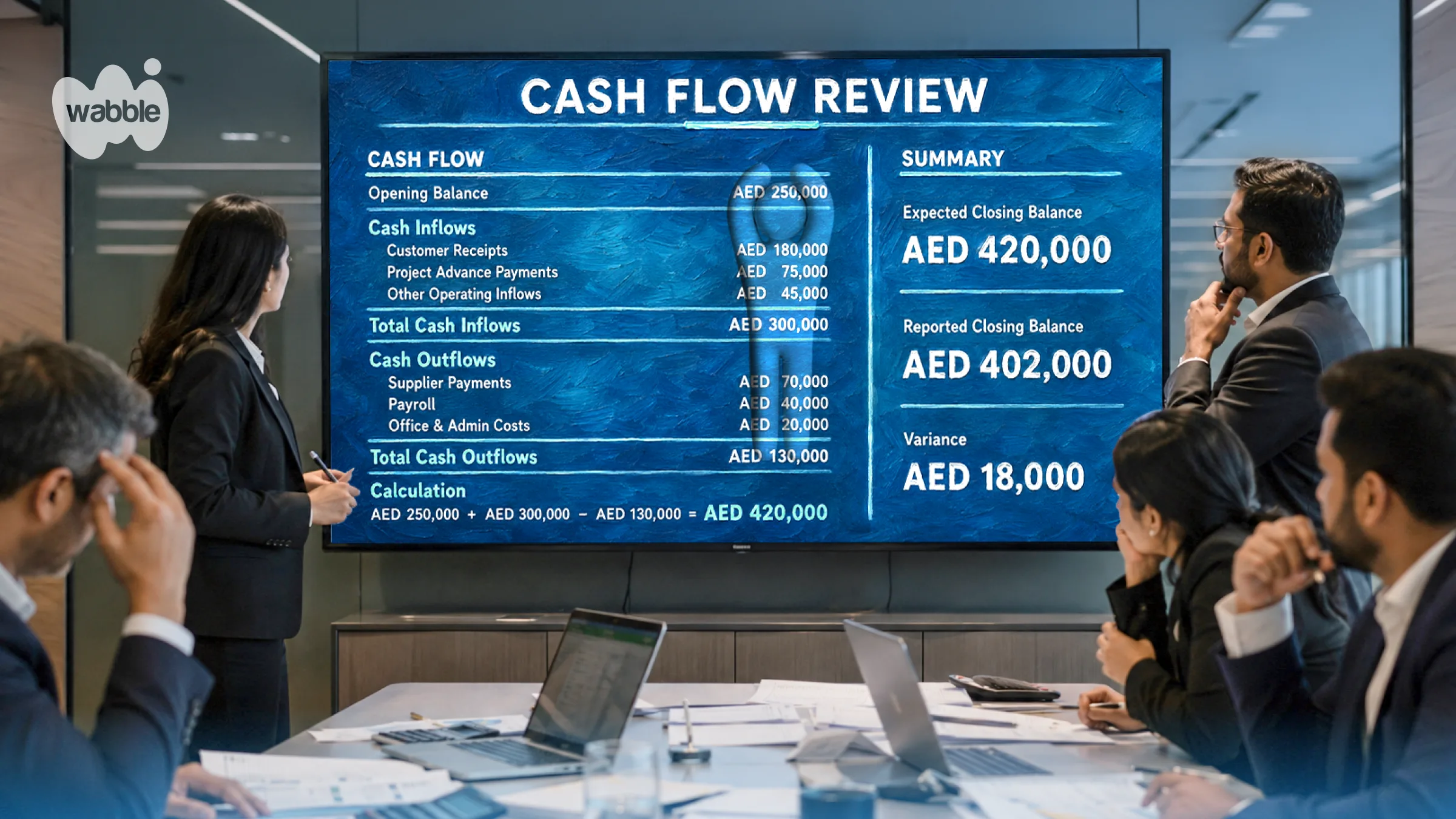

Bank Reconciliation: A Basic Control Every Business Needs

Bank reconciliation is the process of comparing bookkeeping records with actual bank account activity.

This is one of the most important bookkeeping tasks because it helps identify:

- Missing transactions

- Duplicate entries

- Bank charges not yet recorded

- Uncashed cheques

- Data entry errors

- Potential fraud or unauthorized transactions

For example, a business may record a customer payment but later discover the funds were never received. Regular reconciliation helps detect these issues before they affect financial reporting.

Most small businesses benefit from performing bank reconciliations at least monthly. Businesses with higher transaction volumes may require more frequent reviews.

VAT Recordkeeping Requirements in the UAE

Businesses registered for VAT must maintain sufficient records to support VAT returns.

Important VAT-related documents include:

- Tax invoices

- Tax credit notes

- Import and export documentation

- Purchase invoices

- VAT return submissions

- Supporting accounting records

The UAE Federal Tax Authority requires businesses to retain records for prescribed periods under applicable tax regulations. Incomplete VAT documentation can lead to difficulties during audits and may expose businesses to penalties.

Good bookkeeping helps ensure VAT collected and VAT paid are recorded accurately throughout the year rather than reconstructed at filing time.

How Corporate Tax Has Increased the Importance of Bookkeeping

The introduction of UAE corporate tax has increased the need for accurate accounting records.

Corporate tax calculations rely on financial information generated from bookkeeping records. Errors in revenue recognition, expense recording, or transaction classification can affect taxable income calculations.

Businesses that maintain organized books throughout the year are generally better prepared for:

- Corporate tax registration and filings

- Financial statement preparation

- Tax assessments

- External reviews and audits

Even smaller businesses should establish consistent bookkeeping practices early rather than waiting until year-end reporting deadlines approach.

Building Strong Bookkeeping Habits for Long-Term Growth

Bookkeeping does not need to be complicated, but it does need to be consistent. Recording transactions promptly, maintaining supporting documentation, reconciling bank accounts regularly, and keeping tax records organized can help small businesses avoid costly mistakes.

For UAE businesses, bookkeeping is more than an administrative task. It supports VAT compliance, corporate tax obligations, payroll administration, and day-to-day financial management. Strong bookkeeping practices give business owners a clearer view of their operations and provide the records needed to meet regulatory requirements with confidence.

Fadhiya Mushthakh

COO and Co-founder of Wabble Inc., where she focuses on business operations, partnerships, and marketing strategy. Her background spans SaaS marketing and operational execution, working closely with businesses across different industries in the GCC.