A cash flow report can appear complete while the closing balance does not match. A supplier invoice can look legitimate even though it has already been paid. A bank balance can appear healthy while unrecorded obligations are waiting in the background.

None of these problems necessarily looks serious at first glance. That is precisely why they can remain unnoticed.

The consequences can extend beyond administrative inconvenience. Weak documentation can complicate VAT records. Poor transaction tracking can affect corporate tax preparation. Payroll errors can create employee issues and, where applicable, WPS-related problems. Delayed reconciliations can leave owners making decisions from numbers that have not been properly checked.

The difficulty is that these problems rarely announce themselves. They blend into normal work until their combined effect becomes expensive.

Duplicate invoices can quietly drain cash

Duplicate invoices are a simple example of a problem that can remain unnoticed for longer than expected.

A supplier may resend an invoice after following up for payment. The second copy may arrive through a different channel, perhaps directly to an employee rather than the finance team. Someone may enter the same invoice twice with slightly different descriptions or dates. If the business relies on manual checks, both entries can move through the payment process.

The result may be a duplicate payment, but the problem does not always end there. Recovering the money requires someone to identify the error, contact the supplier, confirm the overpayment, request a refund or credit, and track the correction.

Even when the amount is eventually recovered, the business has temporarily lost access to cash and spent additional time correcting an avoidable mistake. Duplicate invoices become harder to detect when supplier records are inconsistent, invoice numbers are entered incorrectly, or different people handle invoice receipt, approval, and payment. A monthly review may eventually find the issue, but by then the cash has already left the bank account.

The practical control is straightforward: every invoice should have a clear record, a consistent supplier reference, evidence of approval, and a check against previous entries before payment.

Missing receipts become bigger problems later

A missing receipt rarely feels urgent when the transaction happens. Someone pays for fuel, travel, office supplies, a client expense, or a business subscription and promises to send the document later. Later becomes month-end.

The finance team then has a bank or card transaction without enough supporting information. They may know how much was spent but not have the documentation needed to confirm the nature of the expense or its tax treatment.

In the UAE, record quality matters for VAT and corporate tax purposes. Businesses need appropriate supporting records for transactions and should not assume that a bank statement alone provides all the information required for accounting or tax treatment.

Missing documents also create uncertainty. Was the purchase entirely business-related? Does the amount include VAT? Is there a valid tax invoice? Which project, department, or customer should carry the cost?

One missing receipt may require a few messages to resolve. Dozens of missing receipts can turn month-end into a document collection exercise.

The longer the delay, the harder the transaction becomes to reconstruct accurately. People forget what they purchased, suppliers become harder to contact, and supporting documents disappear into inboxes and messaging apps.

Unapproved spending weakens control over cash

Small businesses often rely on informal approval. A manager sends a message saying, “Go ahead.” An employee buys something urgently and explains it later. A recurring subscription continues because nobody has reviewed whether the business still needs it.

Individually, these expenses may be reasonable. Collectively, uncontrolled spending makes cash harder to manage.

The problem becomes especially visible when several people can commit company funds without a clear approval process. Finance may only discover the expense when an invoice arrives or money leaves the bank account.

At that point, the spending decision has already been made.

A useful approval process does not need to make every purchase slow. It should answer basic questions before significant spending occurs: who requested it, what it is for, who approved it, how much was approved, and where the supporting document is stored.

Without those answers, finance teams spend time reconstructing decisions after the fact. Owners also lose a clear view of committed spending because some obligations exist outside the accounting records.

That gap matters when cash is tight. A bank balance may look healthy even though supplier payments, payroll, tax obligations, and other approved expenses are already approaching.

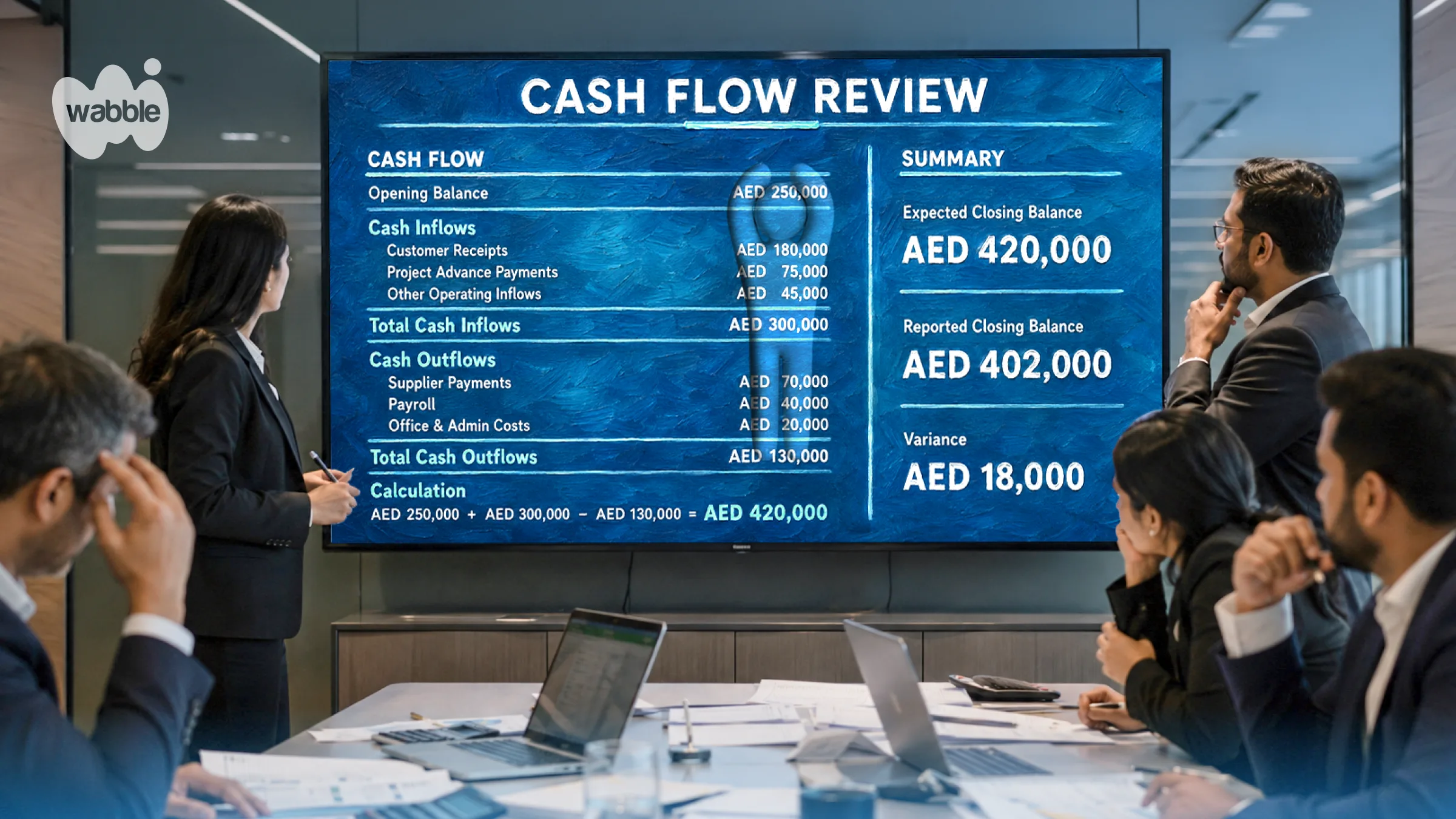

Delayed reconciliations allow errors to stay hidden

Bank reconciliation is one of the clearest ways to find problems that are otherwise easy to miss. The accounting records may show one balance, while the bank shows another. The difference could come from an unrecorded fee, a duplicate transaction, an unmatched customer payment, an incorrect entry, or a payment that has not yet cleared.

If reconciliation happens promptly, the investigation is usually easier. The transactions are recent, supporting documents are easier to find, and the people involved are more likely to remember what happened. When reconciliation is delayed for weeks or months, small discrepancies accumulate.

This affects more than the bank balance. If transactions are missing or recorded incorrectly, management reports may also be wrong. Revenue, expenses, receivables, payables, and cash positions can all be affected by unresolved entries.

A business may then make decisions using figures that appear complete but have not been fully checked.

Regular reconciliation provides a basic test of whether financial records agree with external evidence. When that test is repeatedly postponed, hidden finance problems get more time to grow.

Small finance problems often appear together at month-end

The impact of these issues becomes most visible during month-end close.

The finance team begins reviewing the accounts and discovers missing receipts, unexplained payments, unreconciled balances, invoices waiting for approval, customer payments that have not been matched, and spreadsheet adjustments that need to be understood. Each task takes time. More importantly, many depend on people outside finance.

An employee must find a receipt. A manager must confirm an expense. A supplier must resend an invoice. A customer payment needs to be identified. Someone must explain why a spreadsheet number was changed. Month-end then becomes a chase for information.

This is why a business can have a capable finance team and still experience delayed reporting. The delay may come from dozens of small unresolved items scattered throughout the month.

The same pattern affects cash management. Duplicate payments reduce available cash. Delayed customer payment follow-up slows collections. Unrecorded expenses distort the expected cash position. Unmatched transactions make the bank balance harder to interpret. By the time the problem becomes visible in a report, it may have existed operationally for weeks.

Finding hidden finance problems before they accumulate

The best time to deal with a small finance issue is when the transaction is still recent. Invoices should be checked before payment. Receipts should be collected close to the date of purchase. Spending should have clear approval. Reconciliations should happen regularly. Manual adjustments should be documented and investigated when they repeat.

The objective is not to create a heavy control process around every transaction. It is to stop ordinary exceptions from disappearing into the background.

Small hidden issues create big finance pain because they compound. One missing document is manageable. A month of missing documents delays the close. One incorrect payment can be corrected. Repeated payment errors weaken cash control. One spreadsheet adjustment may be necessary. A reporting process built on unexplained adjustments becomes difficult to trust.

Some finance problems are easier to catch when you know where to look. We’re working on making that a little easier with Wabble.

Fadhiya Mushthakh

COO and Co-founder of Wabble Inc., where she focuses on business operations, partnerships, and marketing strategy. Her background spans SaaS marketing and operational execution, working closely with businesses across different industries in the GCC.