AI is becoming increasingly common across finance teams. Transaction categorization, invoice processing, bank reconciliation, expense management, and reporting support now appear in many accounting platforms. Yet despite the growing adoption of AI accounting software, CFOs often approach these systems with caution.

The hesitation is not rooted in resistance to technology. Finance departments have used automation for years. The concern appears when AI begins influencing accounting decisions, financial classifications, approvals, and reporting outcomes that affect compliance, audits, and management reporting.

For finance leaders, the question is simple: can the numbers still be trusted?

Why Trust Matters More Than Speed in Finance

Business functions can tolerate a degree of experimentation. Finance rarely has that luxury. Every VAT return, payroll run, supplier payment, month-end close, and management report depends on data that can be verified and explained. When figures appear incorrect, finance teams must be able to identify where the issue originated and how it affected the records.

An AI tool that saves time during transaction processing may appear valuable. Problems arise when finance teams cannot understand how a recommendation was generated or why a transaction was categorized in a particular way.

A delayed report creates operational inconvenience. An unexplained financial result creates risk. That distinction shapes how CFOs evaluate an AI accounting software.

AI Changes the Nature of Accounting Risk

Traditional accounting errors are usually traceable. A duplicated payment, missing invoice, incorrect VAT code, or reconciliation discrepancy can often be linked to a specific action, user, or process failure.

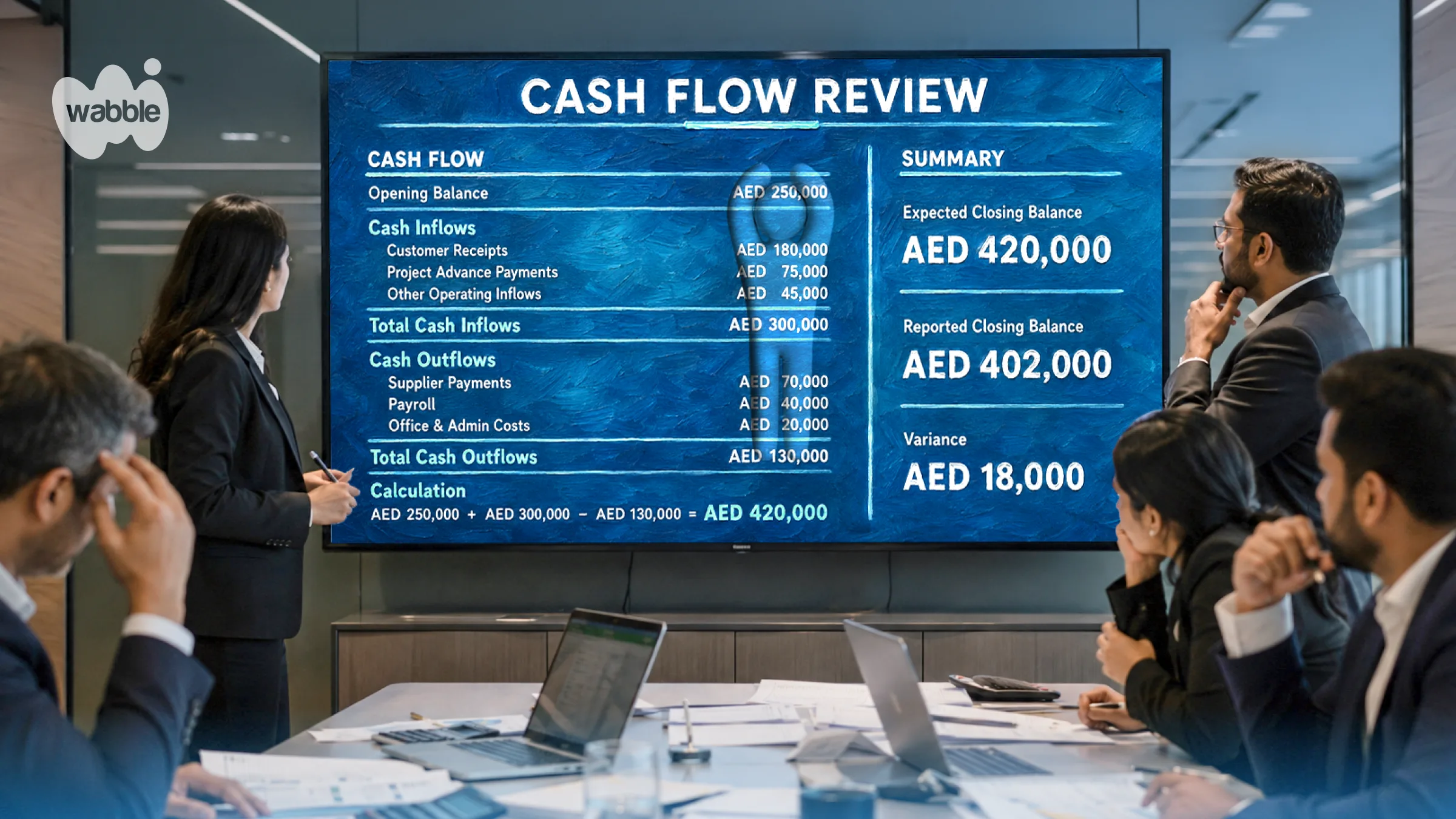

AI introduces a different challenge. Decisions may be influenced by models, recommendations, or automated classifications that are less transparent to finance teams. During routine operations, these issues may go unnoticed. The real test often arrives during month-end close, audits, tax reviews, or board reporting.

A transaction that was automatically categorized months earlier may suddenly require explanation. If finance teams cannot clearly demonstrate how that decision was made, the efficiency gained earlier can disappear during review and investigation.

This concern becomes more significant as AI moves closer to core accounting functions.

Month-End Close Reveals Whether AI Helps or Creates More Work

The month-end close remains one of the clearest indicators of finance process quality. Throughout the month, accounting activities can appear smooth. Transactions are processed, invoices are approved, and expenses are recorded. The pressure arrives when finance teams need complete confidence in the numbers.

This is often when missing supporting documents, reconciliation differences, duplicate entries, and reporting inconsistencies become visible. CFOs evaluating AI accounting software frequently ask whether the technology reduces the work required during close periods or simply shifts that work elsewhere.

An automated classification may save several seconds when a transaction enters the system. If that classification later requires extensive review, correction, or explanation, the benefit becomes less clear.

Finance leaders are less interested in isolated automation gains and more interested in whether the overall reporting process becomes more reliable.

Auditability Remains a Core Requirement

Accounting systems serve more than internal finance teams. External auditors, tax authorities, investors, lenders, boards, and regulators may all require evidence supporting financial records.

That is why audit trails remain essential.

When AI participates in financial workflows, finance leaders want visibility into:

- Why a transaction was categorized a certain way

- What information influenced a recommendation

- Who approved exceptions

- When adjustments were made

- How changes affected reporting outcomes

Without clear records, accountability becomes harder to establish.

This concern is particularly relevant in finance because many reviews occur months after the original transaction. Teams need the ability to reconstruct decisions long after they were made.

For CFOs, transparency often matters as much as accuracy.

UAE Businesses Face Additional Compliance Considerations

Finance leaders operating in the UAE evaluate AI through the lens of local compliance requirements.

VAT obligations require businesses to maintain appropriate records and supporting documentation. The introduction of UAE Corporate Tax has added further attention to financial accuracy, documentation, and reporting consistency.

Growing businesses may also need to manage:

- Multi-entity reporting

- Multi-currency transactions

- Cross-border operations

- WPS payroll requirements

- Supplier and customer documentation

Under these conditions, accounting decisions must remain explainable.

An AI-generated recommendation may be useful, but finance teams still need confidence that records can withstand review by auditors, tax advisors, and regulatory authorities when necessary. The Federal Tax Authority's record-keeping requirements make documentation quality an ongoing priority for UAE businesses.

What CFOs Actually Want From AI Accounting Software

Finance leaders are not asking AI systems to replace professional judgment. They are looking for technology that reduces repetitive work without weakening confidence in financial reporting. The most attractive AI accounting tools tend to support finance teams by helping with data entry, transaction matching, anomaly detection, document extraction, and workflow assistance.

What CFOs continue to evaluate is whether the system improves trust in the accounting process.

Questions commonly include:

- Can transactions be traced back to their source?

- Can adjustments be explained months later?

- Can auditors review decisions efficiently?

- Can finance teams verify AI recommendations?

- Can reporting remain consistent across the business?

Those concerns apply equally to startups, SMEs, multi-entity organizations, and larger finance teams.

Trust Will Determine the Future of AI Accounting

AI will continue expanding across accounting and finance functions. The productivity benefits are difficult to ignore. For finance leaders, the objective has never been automation alone. It is confidence in the numbers. When AI operates within clear controls, maintains complete audit trails, and allows every financial decision to be traced back to its source, it becomes far easier to trust.

The strongest AI accounting systems are likely to be those that help finance teams work faster without sacrificing accountability, transparency, or oversight. In finance, trust is built through visibility into how decisions are made and how records can be verified. As AI adoption grows, platforms that combine intelligence with traceability will be best positioned to earn that trust, which is precisely the direction that Wabble is taking.

Fadhiya Mushthakh

COO and Co-founder of Wabble Inc., where she focuses on business operations, partnerships, and marketing strategy. Her background spans SaaS marketing and operational execution, working closely with businesses across different industries in the GCC.